This graph is showing the condition of all banks and all types of loans, and the percent of the loans they report as non-performing. I believe the common definition of a non-performing loan is one with the payment at least 90 days overdue, or worse, including pending foreclosures. This shows the banking system is not healthy and could be on a trend to a future banking solvency crisis.

Also, Calculated Risk is writing this week that the number of homes in foreclosure is still increasing. He points out "the combined REO (Real Estate Owned) inventory for Fannie, Freddie and the FHA increased by 22% in Q1 2010 from Q4 2009. The REO inventory (foreclosed homes) increased 59% compared to Q1 2009 (year-over-year comparison)."

In order to stem the rising trend of non-performing loans, banks have to make more loans to credit worthy borrowers. It seems that both personal and commercial borrowers are becoming harder to find. Here is a link to the Economist's View blog and a guest article titled Banks Failing to Lend is Not the Problem. The article presents a varied discussion on solutions to stimulate the flow of primarily commercial credit, including a call for more federal stimulus.

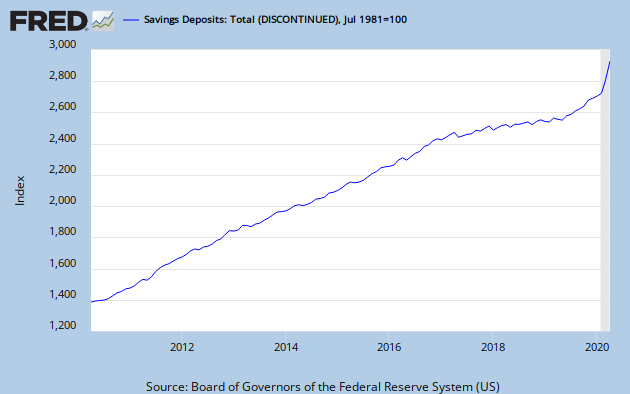

The following graph shows that savings deposits are increasing and that could imply that some people who have been borrowers are slowly becoming savers. Something to keep an eye on.

In my opinion, banks are heading for a crash landing in the not too distant future, just a few years from now. The result will be a new look banking system and getting there is not going to be painless for the US economy. In the short-term meantime, the NYSE is benefiting from the leadership of the financial sector leading the index to higher highs with little change of direction. The larger banks can still make big profits with so much cheap cash available and they are still allowed to trade for themselves and their clients, as if they were investment banks. Scanner